10 Charts to Watch in 2021 [Q1 Update]

- Callum Thomas

- Apr 13, 2021

- 6 min read

Welcome to Q2! Things have moved fast since my original post (both in terms of market movements and the general consensus/sentiment). So I thought it would be helpful to take a quick progress check on the "10 Charts to Watch in 2021".

In the original article I shared what I thought would be the 10 most important charts to watch for multi-asset investors in the year ahead (and beyond).

In this article I have updated those 10 charts, and provided some updated comments.

[Note: I have included the original comments from back at the start of the year, so you can quickly compare what I'm thinking now vs what I said back then]

1. Mega Theme: This basket of ideas has been performing nicely, perhaps a little too nicely - indeed the breadth of performance almost got a little too overheated, and a couple of themes within it have taken a breather. I think it's quite possible this basket does take a breather after such a roaring snap-back. Yet, the valuation picture remains positive, and I have yet to find good reason to discard any of the individual ideas - so aside from a possible consolidation/brief give-back, basically stay the course on this one.

"In the last regular edition of the Weekly Macro Themes report of 2020, I decided to combine all my big ideas into one “mega theme” given some of the echoes across the ideas in terms of price action and macro drivers. The result is this interesting chart which looks to be either at or near the bottom of a long-term secular trend, and the start of at least a short-term cyclical upturn."

2. Monetary Policy (limits): Things have moved on a bit on the policy front, and indeed in terms of recovery there has been a lot more action (and talk) on fiscal policy. We likely see fiscal policy doing more heavy lifting, and so far there has been increasing focus on infrastructure and energy transformation... interesting stuff.

"The policy response to the pandemic was historic in terms of its speed, magnitude, and coordination across countries and between fiscal and monetary. But this chart perhaps highlights one limitation of monetary policy, the tag line is “interest rates are low, but good luck getting a loan” (given how much banks tightened up on lending standards). One thing on my mind is a possible passing of the torch from monetary policy to fiscal policy – as that’s going to be the thing that will achieve a more balanced and more transformative impact in the recovery."

3. Global Trade Rebound: Global trade has made a rapid recovery, with global trade volumes easily clearing pre-pandemic levels. The snapback has been so rapid (recovering demand, changing demand) in fact that shipping costs have surged - e.g. as an interesting anecdote, the price of humble wooden shipping pallets has doubled.

"The global economic shutdown saw an abrupt collapse in trade growth. But since then we have seen clear green shoots and the leading indicators point to an acceleration and continuation of the global trade growth rebound into 2021."

4. Global Backlogs: As such, it should be no surprise to see that the backlogs/supply chain disruption issue has only gotten worse... and boats getting stuck in canals don't exactly help the situation! As a result of tight inventories, lengthy shipping delays, shortages of parts, logistics challenges, lockdowns, and surging freight rates, we have started to see wider pricing pressure come through. Thus inflation risks remain very much upward skewed in the near-term [but as noted in my Q2 Strategy Pack, medium-term the case for higher inflation is also compelling].

"A nice follow-on, the surge in backlogs (resulting from global supply chain disruption) has 2 key implications: upside risk to inflation, and a likely spike in activity as firms attempt to clear backlogs and restock inventories."

5. Consumer Normalization: Consumer sentiment is steadily recovering worldwide as vaccines are rolled out (worldwide vaccinations are running at a pace of 17m/day at the time of writing), asset prices steadily push higher (housing + equities), and at least according to the stats: *in aggregate* consumers are flush with cash.

"Consumer moods remain depressed *outside of China*. This chart provides a sort of playbook for the rest of the world, as well as a key means of keeping track of normalization, and a nod to a potential consumer boom post-vaccine."

6. US vs the Rest of the World: As alluded to in the first chart, there had been some fairly decent moves e.g. the swift downward move in the US dollar which saw nearly every analyst & their dog turning bearish. Even global vs US equities relative performance had begun to turn the corner... but we're seeing a bit of giveback on both fronts. I say stay the course on both: the case remains compelling, especially for global vs US equities.

"All the key pieces of the puzzle seem to be falling into place for the rest of the world to start outperforming vs US equities. Along with that, I expect ongoing weakness in the US dollar."

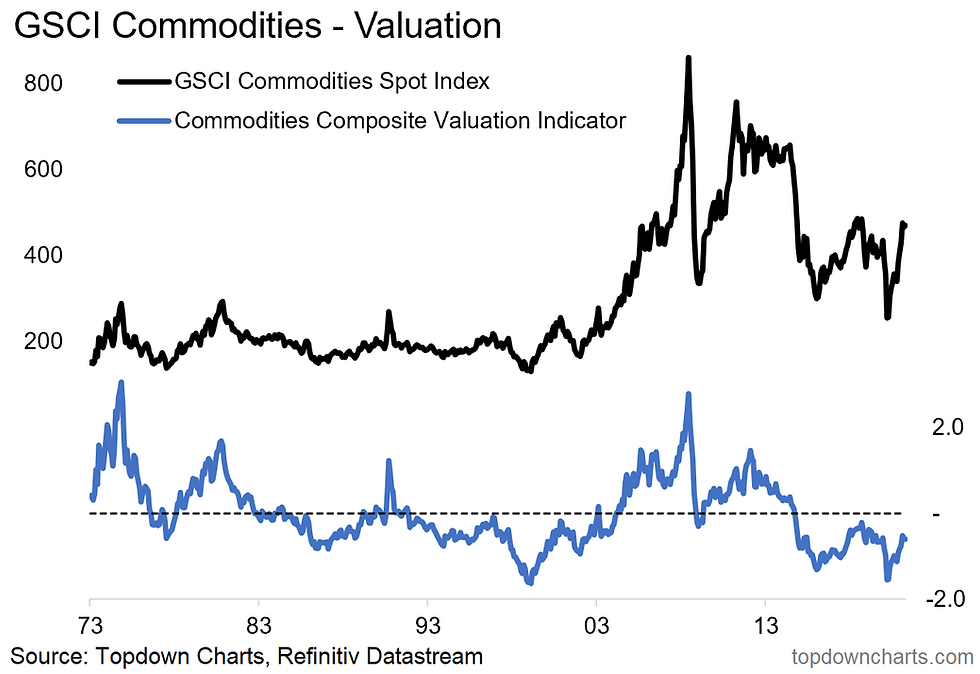

7. Commodities: The case for commodities remains very compelling medium/long-term for a decent list of reasons (I have charts, just ask me)... BUT: short-term sentiment & positioning have become very stretched (and actually starting to rollover), meanwhile ...although the pandemic looks to be turning the corner, it is still here, and there are still downside risks. Furthermore, there is clearly a backlog/supply chain disruption premium in commodities - if that gets resolved quickly then that premium comes back out and prices go down short-term. Remain bullish medium/long-term but mindful of the short-term risk outlook.

"Given cheap valuations, a prolonged period of weak capex (i.e. futures supply tailwinds to price), pandemic disruption, an expected weaker USD, and economic recovery (with potential overshoot), remain decidedly bullish here."

8. Real Yields: Adroit observers will notice that I re-drew the line here... previously I had it lower down as support, but now I think this overhead resistance area is the more important thing to pay attention to. I still see the risks clearly skewed to the upside for real yields given the evolving macro-thematic picture, but that line is meaningful: it's a clear and logical resistance level that will need to be cleared before any real upside in real yields is on the table. And as noted, with various risk bogeymen still lurking, that glass ceiling could prove tough to break in the short-term.

"In my view the two key drivers of US real yields are risk sentiment and growth expectations. Naturally on both fronts it was entirely rational to see real yields plunge this year. Going forward I expect improved risk sentiment and a rebound in growth expectations; therefore I expect higher real yields (and nominal yields)."

9. Crude Oil vs Gold: One of my fav charts of last year - was such a non-consensus call at the time, perhaps less so now as the market has come round and realized how big the relative price has moved. Strictly speaking it's still "cheap" vs long-term average. Stay the course... but that has been one BIG move already.

"The logical next question should then be “what about gold?”. All else equal, a prospective environment of higher real yields would present a headwind to the consensus and crowded long gold trade. Aside from that, I believe a prospective passing of the torch from monetary to fiscal in the US is strong possibility (incoming Treasury Sec. Yellen has a deep appreciation for the limits of monetary policy and the need for fiscal policy to do more of the heavy lifting). This along with post-vaccine normalization should disproportionately benefit oil at the expense of gold, so I suspect we see some mean reversion in this chart."

10. China: Despite a circa -10% correction, China A-shares remain above their 200dma and bigger picture; above their long-term uptrend line. To update the view, sentiment on Chinese assets remains broadly negative in the US as anti-China politics linger heavy despite the change in President (seems to have become a relatively bi-partisan issue at this point). Aside from that though, the earnings/macro pulse has turned up materially, and although the overall policy picture is a bit more muted this time around - it is still a tailwind at this point. Yet valuations are not exactly cheap, indeed, I see better value in EM ex-Asia (as you might have picked-up in the first chart).

"Last but not least is China. While I continue to watch a wide range of indicators, one in particular focus will be China A-shares, particularly as they brush up against a key overhead resistance level, and as policy makers in China possibly move toward actually tightening monetary policy in 2021. Indeed, in many respects, I suspect it will be more of China zigging, while the rest of the world is zagging. In any case, I remain convinced that it is still one of the most important economies and markets to watch in understanding the global macro/market picture."

Summary and Key Takeaways:

Monetary policy remains of critical importance, but expect less monetary and more fiscal stimulus going forward.

Anticipate follow-through on the global economic recovery as stimulus, green shoots, and clearing of backlogs coalesce.

Clear upside risk to inflation near-term given backlogs, base effects, and commodities

Expect the risk-on/reflation/recovery macro environment helps some of the previously unfavored asset classes, and drives rotation within and across markets.

Anticipate a more nuanced approach to global equity allocations will be more appropriate than just market cap weights: fade passive.

Likely further upside for commodities, higher bond yields, and weaker USD.

Still plenty of interesting opportunities (and risk) out there!

Best regards,

Callum Thomas

Head of Research and Founder of Topdown Charts

Follow us on:

Comments