Defensive Value: The Safety Trade of 2022

- Mike Zaccardi, CFA, CMT

- May 10, 2022

- 3 min read

Healthcare, Staples, and Utilities continue to outperform as selling intensifies in the growth style

Investor positioning is still light in the space – even after a year of alpha

While absolute valuations have turned somewhat pricey, the defensive supersector shows decent relative value (along with strong price momentum)

The global stock market is off to an awful start this year. No two ways about it. But it’s not as if everything has gone down together. There have been several niches that have softened the blow relative to huge drops in areas like big cap tech, homebuilders, retail, biotech, China, and long-term bonds.

A Safe Place

Defensive value sectors – Healthcare, Consumer Staples, Utilities – are doing ok so far in 2022. Healthcare (XLV) is the worst performer among the three with an 8% year-to-date decline, but that is due in part to biotech's (IBB) 26% freefall. Consumer Staples (XLP) is down just 51 basis points while Utilities (XLU), despite rising interest rates, is up 1% for the year. These safe haven plays indicate a risk-off atmosphere.

Pay Me Now

Also driving the flight to stability is the demand for cash flows now. The trio of defensive value sectors delivers dividends and near-term profits. As interest rates rise, the discounting effect of future cash flows means that growth stocks - those that hope to one day turn very profitable – are worth less, and impart a tightening effect on the economy (e.g. see leading indicators). Our Weekly Macro Themes report revisits a play about which we have been optimistic since March of last year.

Sticking With an Overweight

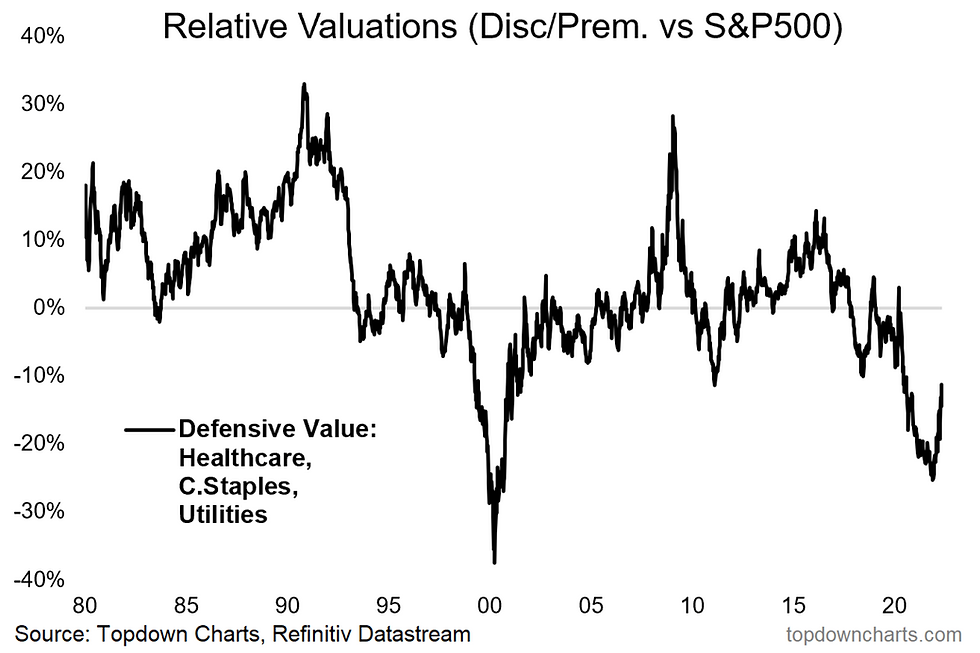

It’s rare to have a broad set of sectors remain a tactical play for beyond 12 months, but we assert that the case for an overweight to defensive value remains intact. Despite sharp outperformance this year, the three sectors continue to trade at a healthy discount vs the S&P 500 (though the valuation gap has narrowed in recent months).

Not Super Cheap, But Cheaper Than the Rest

From an absolute valuation perspective, the defensive supersector has actually turned a bit expensive, however. On their own, Healthcare/Staples/Utes are near 1.5 standard deviations above their long-term average valuation. That’s materially more than, say, cyclical value sectors (Energy & Financials). Versus the S&P 500, though, defensive value is slightly more than 10% cheaper while cyclical value trades at a nearly 40% discount despite nice alpha YTD.

Featured Chart: Defensive Value Relative Valuation

Light Positioning

The kicker that makes us reiterate a bullish outlook is that defensive value continues to track near all-time lows in terms of market cap representation. And investor allocations are historically light. Thus, a contrarian overweight setup remains on solid footing. It’s likely that as volatility persists throughout 2022, investment managers and advisors will shift away from volatile growth shares and into the perceived safety of large-cap value sectors.

Investors Not Giving Up on Growth

The trend will lose momentum at some point, of course, but that likely won’t happen until we see valuations in big-cap tech come way in. We also must see more signs of capitulation from those areas. With money continuing to flow into funds like ARKK, we obviously aren’t there yet. What's more, investor allocations to equities remain high, despite all the fear.

Bottom Line: We remain bullish on defensive value sectors despite their strong rally over the last 14 months since we initiated the call. The sectors’ original value/sentiment/positioning case still holds. Recent performance and building momentum should draw more investor flows to the space.

Follow us on:

Substack https://topdowncharts.substack.com/

In Buckshot Roulette, I realize I’ve been counting shells wrong the entire round. Correcting that mistake changes my next move.

Great insights! Defensive value sectors like Healthcare, Staples, and Utilities really show their strength during uncertain times, offering stability when growth stocks struggle. I appreciate the breakdown on valuations and momentum. For businesses seeking credibility, exploring the best Wikipedia page creation service can also enhance visibility and trust.